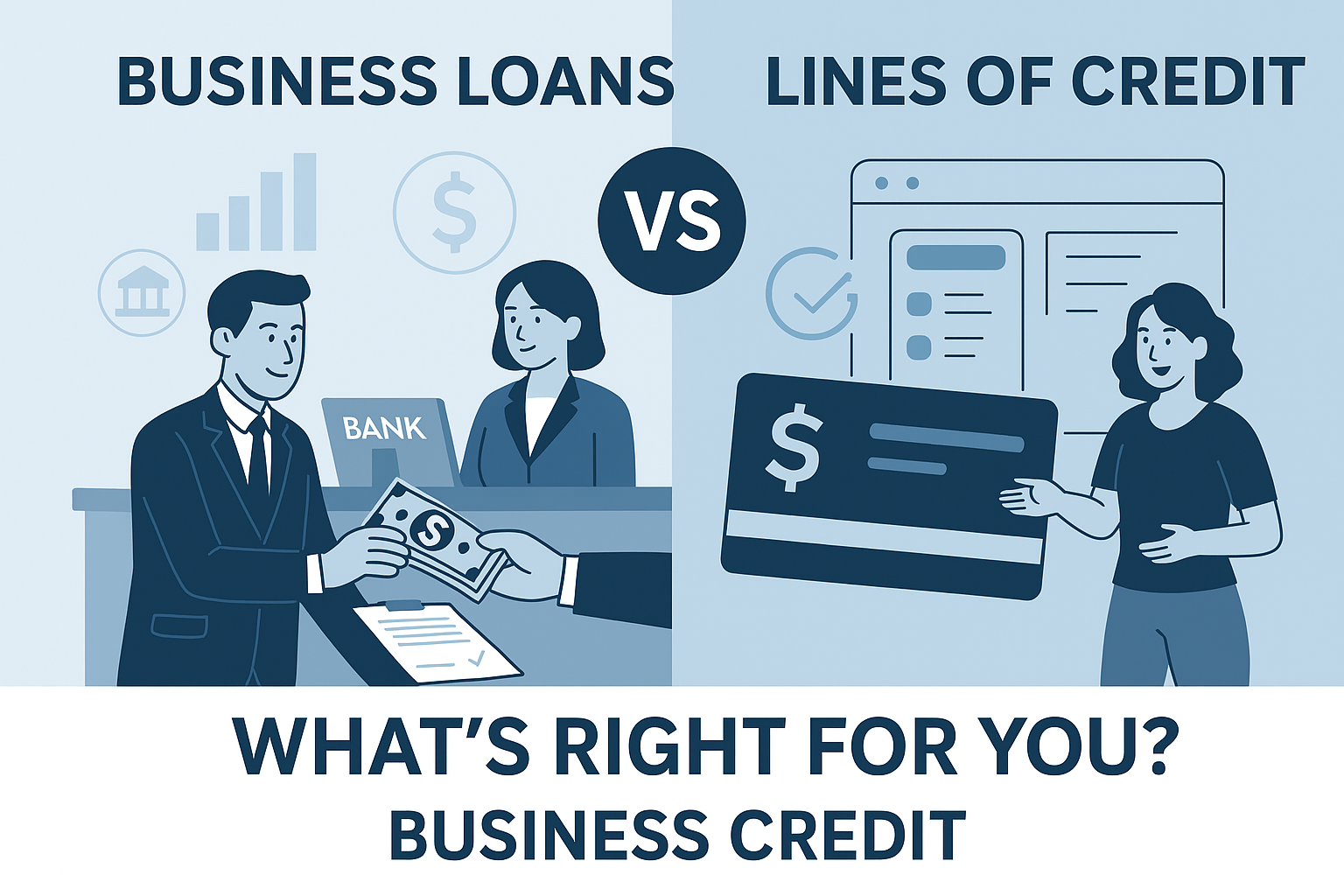

Business Loans vs. Business Lines of Credit: Which is Right for You?

Published on April 2, 2025

Written by

Sophia Patel

Working Capital Consultant

Key Takeaways

- Business loans provide a lump sum with fixed repayment terms, ideal for specific, one-time investments

- Business lines of credit offer flexible access to funds as needed, with interest paid only on what you use

- Loans typically have lower interest rates but less flexibility than lines of credit

- Lines of credit work best for managing cash flow gaps and unexpected expenses

- Your business's age, financial health, and specific needs determine which option fits best

- Many businesses benefit from having both financing tools available

Understanding Business Loans: Structure, Types, and Uses

Business loans form the backbone of most companies' growth strategies. These financial tools give businesses access to a set amount of money paid in a lump sum. The borrower then repays this amount plus interest over a predetermined period.

The structure of a business loan is straightforward. You receive the entire loan amount upfront and start making payments based on an agreed schedule. Most business loans include:

- Principal amount (the sum borrowed)

- Interest rate (fixed or variable)

- Term length (typically 1-10 years)

- Payment schedule (usually monthly)

- Any collateral requirements

Tom runs a small manufacturing business and needed $75,000 for new equipment. He got a business term loan with a 6% interest rate and 5-year term. His monthly payments stay consistent at $1,450, making budgeting simple. The predictability helped his business plan cash flow around the purchase.

Business loans come in several varieties, each designed for specific needs:

| Loan Type | Best For | Typical Terms |

|---|---|---|

| Term Loans | Major purchases or investments | 1-10 years, fixed payments |

| Equipment Financing | Machinery and equipment purchases | Term matches useful life of equipment |

| SBA Loans | Businesses that may not qualify for traditional loans | Longer terms, government-backed |

| Working Capital Loans | Day-to-day operations | Shorter terms, quick funding |

Business loans work best for specific, one-time funding needs. The rigid structure of loans means you know exactly what you're getting and what you'll pay. This predictability helps many business owners sleep better at night.

I've worked with clients who leveraged term loans to fund major expansions. One restaurant owner used a business loan to open a second location. The fixed payment schedule aligned perfectly with her projected revenue growth. She knew exactly how much the expansion would cost each month, which eliminated financial surprises during a critical growth phase.

The benefits of business loans include:

- Lower interest rates compared to most other financing options

- Predictable payment amounts for easier budgeting

- Potential tax benefits (interest may be deductible)

- Building business credit with timely payments

However, loans come with limitations. Once you receive the funds, you can't borrow more without applying for another loan. You'll pay interest on the full amount from day one, even if you don't immediately use all the money. And if your needs change, the loan terms typically remain fixed.

Exploring Business Lines of Credit: How They Work

A business line of credit functions more like a credit card than a traditional loan. It provides access to a pool of funds you can draw from as needed, up to a predetermined limit. You pay interest only on the amount you use, not the entire credit line.

The structure typically includes:

- Credit limit (maximum amount available)

- Draw period (time during which you can borrow)

- Repayment terms (may include minimum monthly payments)

- Interest rates (applied only to borrowed amounts)

- Renewal options (many lines can be renewed after the draw period)

Sarah owns a seasonal retail business with fluctuating inventory needs. She secured a $50,000 line of credit but only draws funds during her busy season. One month she borrowed $20,000 for inventory, paid it back when sales increased, then later drew $15,000 for an unexpected repair. She paid interest only on what she used, when she used it.

Business lines of credit offer remarkable flexibility. They serve as a financial safety net, ready when you need them but not costing you when you don't. This makes them ideal for businesses with variable cash flow or unexpected opportunities.

Lines of credit fall into two main categories:

- Secured lines require collateral (like inventory or equipment) and typically offer higher limits and lower rates

- Unsecured lines don't require specific collateral but may have lower limits and higher rates

From my experience helping small businesses manage their finances, lines of credit prove invaluable during growth phases. One contractor client used his line to purchase materials for new projects before receiving customer deposits. This flexibility allowed him to take on larger jobs without cash flow constraints.

The key benefits of business lines of credit include:

- Pay interest only on what you use

- Borrow and repay repeatedly during the draw period

- Access funds quickly when opportunities arise

- Create a safety net for unexpected expenses

- Improve cash flow management

The main drawbacks involve higher interest rates than term loans and the temptation to rely too heavily on borrowed funds. Some lines also require annual renewal, which means your access to funds isn't guaranteed forever.

Direct Comparison: Loans vs. Lines of Credit

When comparing business loans to lines of credit, several key differences emerge that can help determine which option best suits your needs.

Structure and Flexibility

Business loans provide a single lump sum with a fixed repayment schedule. You know exactly how much you'll receive and what you'll pay each month. Lines of credit offer revolving access to funds, with the ability to borrow, repay, and borrow again as needed.